Ulcer Index

The ulcer index is a stock market risk measure or technical analysis indicator devised by Peter Martin in 1987,[1] and published by him and Byron McCann in their 1989 book The Investors Guide to Fidelity Funds. It's designed as a measure of volatility, but only volatility in the downward direction, i.e. the amount of drawdown or retracement occurring over a period.

Other volatility measures like standard deviation treat up and down movement equally, but a trader doesn't mind upward movement, it's the downside that causes stress and stomach ulcers that the index's name suggests. (The name pre-dates the discovery, described in the ulcer article, that most gastric ulcers are actually caused by a bacterium.)

The term ulcer index has also been used (later) by Steve Shellans, editor and publisher of MoniResearch Newsletter for a different calculation, also based on the ulcer causing potential of drawdowns.[2] Shellans index is not described in this article.

Contents |

Calculation

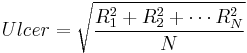

The index is based on a given past period of N days. Working from oldest to newest a highest price (highest closing price) seen so-far is maintained, and any close below that is a retracement, expressed as a percentage

For example if the high so far is $5.00 then a price of $4.50 is a retracement of −10%. The first R is always 0, there being no drawdown from a single price. The quadratic mean (or root mean square) of these values is taken, similar to a standard deviation calculation.

The squares mean it doesn't matter if the R values are expressed as positives or negatives, both come out as a positive Ulcer Index.

The calculation is relatively immune to the sampling rate used. It gives similar results when calculated on weekly prices as it does on daily prices. Martin advises against sampling less often than weekly though, since for instance with quarterly prices a fall and recovery could take place entirely within such a period and thereby not appear in the index.

Usage

Martin recommends his index as a measure of risk in various contexts where usually the standard deviation (SD) is used for that purpose. For example the Sharpe ratio, which rates an investment's excess return (return above a safe cash rate) against risk, is

The ulcer index can replace the SD to make an ulcer performance index (UPI) or Martin ratio,

In both cases annualized rates of return would be used (net of costs, inclusive of dividend reinvestment, etc.).

The index can also be charted over time and used as a kind of technical analysis indicator, to show stocks going into ulcer-forming territory (for one's chosen time-frame), or to compare volatility in different stocks.[3] As with the Sharpe Ratio, a higher value is better than a lower value (investors prefer more return for less risk).

References

- ^ Peter Martin's Ulcer Index page

- ^ Pankin Managed Funds, client newsletter 3rd Quarter 1996, Questions and Answers

- ^ Discovering the Absolute-Breadth Index and the Ulcer Index at Investopedia.com

Further reading

Related topics

Books

- The Investor's Guide to Fidelity Funds, Peter Martin and Byron McCann, John Wiley & Sons, 1989. Now out of print, but offered for sale in electronic form by Martin at his web site [1].

External links

|

||||||||||||||||||||||||||||||||||||||